26

Apr

Maximize trading performance by optimizing your algorithms

TL;DR:

- Continuous optimization adapts trading systems to changing market conditions for sustained performance.

- Overfitting during optimization can cause poor live results; validation across multiple data sets is essential.

- Disciplined, periodic reviews and objective metrics ensure algorithmic strategies remain effective over time.

Automated trading promises freedom, consistency, and profit, but that promise has a catch. Plug in an expert advisor (EA) and walk away? Many traders try exactly that, only to watch their account bleed slowly as market conditions shift and their algorithm keeps firing trades designed for a world that no longer exists. The truth is that automation is only the starting point. What separates profitable algorithmic traders from frustrated ones is a deliberate, disciplined approach to optimization. This guide breaks down what optimization really means, why it matters, and exactly how to do it right in the Forex and gold markets.

Table of Contents

- What does it mean to optimize trading algorithms?

- Key benefits of optimizing your trading algorithms

- Common pitfalls: Overfitting and false confidence

- Practical steps to optimize trading algorithms effectively

- Why algorithm optimization is the real edge, beyond technology

- Unlock your trading edge with proven tools and resources

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Optimization drives results | Automated algorithms require regular optimization to stay profitable and reliable. |

| Overfitting is a hidden danger | Optimizing for past performance alone often backfires in live trading. |

| Validation builds trust | Out-of-sample testing and adaptive techniques strengthen algorithm performance. |

| Practical steps matter | A clear workflow and objective benchmarks are essential to effective optimization. |

What does it mean to optimize trading algorithms?

Let’s get the definition clear. Algorithm optimization is the process of systematically tuning, testing, and adapting your trading system so it continues to deliver strong risk-adjusted returns across changing market conditions. It is not a one-time setup task. It is an ongoing discipline.

Basic automation means your EA executes trades based on a fixed set of rules without you sitting at the screen. That part is valuable. You get speed, consistency, and freedom from emotional decision-making. But automation alone does not protect you from a strategy that has stopped working. Markets evolve. Volatility regimes shift. Correlations between currency pairs and gold change. An algorithm that crushed it during trending 2023 conditions may bleed capital in a choppy, low-volume 2026 range market.

Optimization fills that gap. It involves revisiting your algorithm’s core parameters, such as entry signals, stop-loss widths, take-profit levels, lot sizing, and time filters, and testing whether those parameters still hold up under current and historical conditions. You are not guessing. You are measuring.

Here is what good algorithm optimization actually covers:

- Parameter tuning: Adjusting values like moving average periods, RSI thresholds, or ATR multipliers to find configurations that produce better performance metrics.

- Backtesting over multiple windows: Running the algorithm against historical data from multiple distinct time periods, not just one favorable stretch.

- Out-of-sample (OOS) validation: Testing the refined parameters on data the algorithm was never trained on, confirming the results are real and not just fitted to the past.

- Forward testing: Running the updated algorithm on a demo account in live conditions before deploying real capital.

- Regime analysis: Checking how the strategy performs across different market environments, trending, ranging, and high-volatility sessions.

One of the most important reasons to optimize is bias removal. Mechanical systems for gold trading eliminate human biases like recency bias and confirmation bias, ensuring consistent execution across market conditions through rigid rules and backtesting over diverse periods. That consistency is precious, but it only holds if the rules are kept current.

The algorithmic trading benefits extend well beyond execution speed. They include the ability to test ideas against years of data in minutes. That same power gives you the infrastructure to optimize intelligently rather than guess.

Pro Tip: Before you touch a single parameter, write down your performance goals. What is your target profit factor? What is the maximum drawdown you can tolerate? What does “stable” look like across three different market conditions? Defining these benchmarks upfront keeps your optimization grounded in logic, not wishful thinking.

Understanding the trading system advantages built into a well-structured EA gives you a solid foundation before you start the tuning process.

Key benefits of optimizing your trading algorithms

Once you understand what optimization is, the next question is obvious: is it worth the effort? The short answer is yes, and the numbers back it up.

Adapting to market regimes is one of the biggest wins. A trend-following algorithm calibrated for a bull run in gold will often destroy capital in a sideways market. Regular optimization lets you identify when a strategy’s edge is fading and adjust accordingly, whether that means tightening parameters, reducing position size, or switching to a different strategy module entirely.

Backtesting and OOS validation are your reality check. Any EA can look brilliant on a backtest if you cherry-pick the time period. Gold algo trading benefits from mechanical rules exploiting trends and volatility, but it requires out-of-sample validation across bull, bear, and range conditions to avoid curve-fitting. Putting your optimized strategy through these validation layers dramatically increases the probability that live results will match your expectations.

Preventing profit decay is perhaps the most underappreciated benefit. Even genuinely good strategies lose their edge over time as other market participants discover and trade around the same patterns. Quarterly optimization reviews catch this decay early, before it shows up as a devastating drawdown.

Here is a direct comparison of what optimized and non-optimized algorithms typically look like in practice:

| Metric | Optimized algorithm | Non-optimized algorithm |

|---|---|---|

| Win rate | 55 to 65% | 40 to 50% |

| Maximum drawdown | Controlled (under 15%) | Often exceeds 25 to 30% |

| Adaptability | Adjusted for current conditions | Fixed, regime-blind |

| Strategy longevity | Extended with periodic tuning | Decays within months |

| Real net profit | Consistent over time | Spikes then declines |

Additional benefits traders report after committing to regular optimization include:

- Lower slippage impact through better entry timing calibrated to current volatility.

- Reduced false signals by removing indicators that have stopped predicting price effectively.

- Better capital efficiency from tightening position sizing to match current market dynamics.

- Greater confidence in live trading because forward test results align with backtest results.

Explore specific gold trading system tips to see how these principles apply directly to XAU/USD strategies. You can also dig deeper into the debate between manual vs automated trading to understand where optimization fits in the broader trading workflow.

Common pitfalls: Overfitting and false confidence

Here is where many algorithmic traders trip up badly. Optimization done poorly is worse than no optimization at all. The biggest trap is overfitting, also called curve-fitting. This is when your algorithm’s parameters are tuned so precisely to historical data that they capture the noise of the past rather than the actual signal. The backtest looks extraordinary. The live account does not.

The primary risk is overfitting: strategies fitted too closely to historical data fail in live conditions, shown by smooth backtests versus poor forward performance, and detected via large in-sample versus out-of-sample gaps and high parameter sensitivity.

Recognizing overfitting before you deploy capital is critical. Here is what a robust algorithm looks like compared to an overfitted one:

| Feature | Robust algorithm | Overfitted algorithm |

|---|---|---|

| IS vs. OOS performance | Close and consistent | Major gap, IS much better |

| Parameter sensitivity | Stable across small changes | Collapses with minor tweaks |

| Backtest equity curve | Realistic with drawdowns | Suspiciously smooth |

| Performance across regimes | Works in multiple conditions | Only works in one market type |

| Number of parameters | Minimal and logical | Excessive and arbitrary |

The numbered steps to avoid overfitting and build genuine robustness are:

- Use at least three distinct historical windows when backtesting, not just one long run.

- Always reserve 30 to 40% of your data as out-of-sample and never touch it until final validation.

- Limit the number of parameters you optimize simultaneously. More parameters mean more overfitting risk.

- Apply Monte Carlo simulation to test how the strategy performs across hundreds of randomized variations of its trade sequence.

- Prioritize drawdown control and profit factor over raw profit in your optimization criteria.

- Validate on a live demo account for at least four weeks before committing real capital.

“The goal of optimization is not to create an algorithm that looks perfect on paper. It is to create one that survives and performs in an environment it has never seen before.”

This distinction matters deeply. A strategy with a 70% win rate on a cherry-picked backtest and a 45% win rate on forward testing is not a 70% win rate strategy. It is a warning sign.

Pro Tip: Never optimize purely for maximum profit. Build your optimization criteria around the automated trading workflow metrics that reflect real risk: profit factor above 1.5, max drawdown below your personal risk threshold, and stable performance across at least two different market regimes.

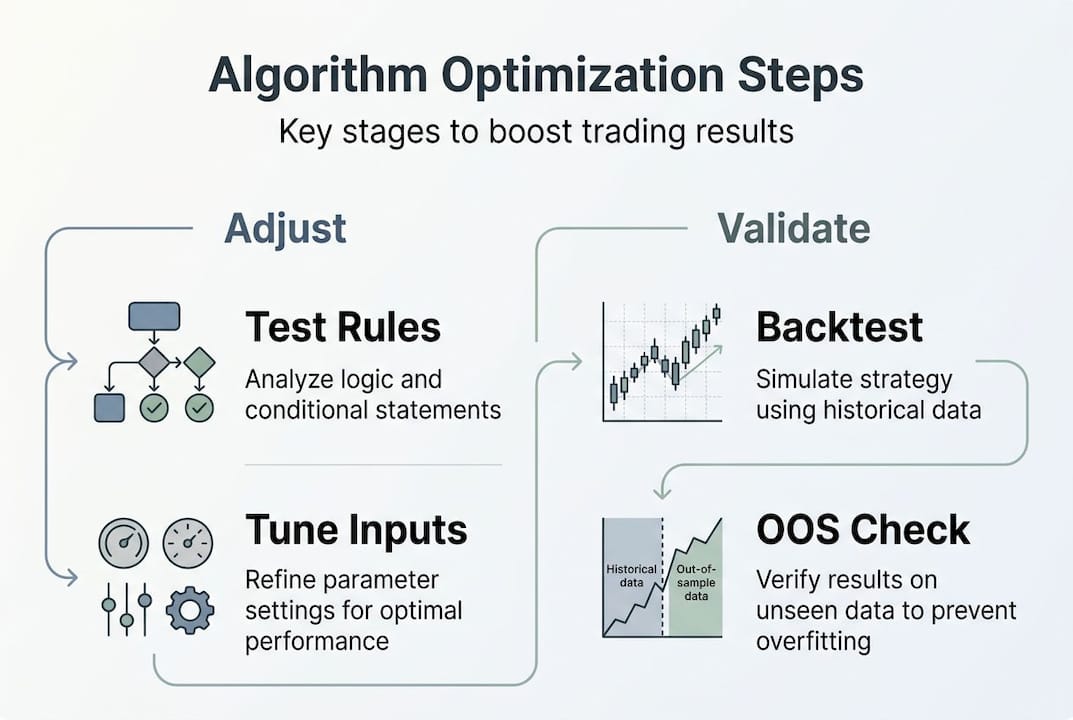

Practical steps to optimize trading algorithms effectively

Now let’s put this into a workflow you can actually follow. Effective optimization is not complex, but it is methodical. Skipping steps is how traders end up with overfitted strategies masquerading as validated ones.

Balance profit and drawdown in optimization criteria, use Monte Carlo for variance testing, and schedule periodic quarterly reviews without making emotional tweaks between cycles. That framework forms the backbone of everything below.

Here is the full optimization checklist:

- Define your success metrics first. Write down your target profit factor, maximum drawdown, minimum trade sample size, and the market conditions you want the strategy to handle.

- Gather quality historical data. Use tick data where possible. Ensure your data covers multiple market regimes including trending periods, ranging periods, and high-volatility events.

- Run an initial backtest on the full in-sample window. Record baseline performance without touching parameters.

- Identify two or three parameters with the most logical impact on performance. Optimize only those. Avoid optimizing more than four parameters at once.

- Validate on the reserved out-of-sample window. If performance drops significantly, you likely have a curve-fitting problem.

- Run Monte Carlo simulations. Generate 500 to 1,000 randomized trade sequence variations and check that the strategy remains profitable across the majority of them.

- Forward test on a demo account for a minimum of four weeks in current market conditions.

- Deploy with reduced position size for the first month of live trading to confirm live results track forward test results.

- Schedule a quarterly review. Set a calendar reminder. Check performance metrics, not the P&L chart. Adjust only if objective metrics indicate degradation.

Machine learning enhancements like attention-LSTM improve Forex predictions, but markets’ increasing efficiency demands adaptive retraining. This is an important nuance: even ML-powered EAs require periodic retraining to remain effective. The market does not stay still just because your algorithm does.

Practical tools that support this process include MetaTrader’s built-in Strategy Tester, third-party backtesting platforms with Monte Carlo modules, and forex gold trading automation resources that walk you through the technical side of deploying and testing EAs on MT4 and MT5.

Pro Tip: Schedule your quarterly review on a specific date and treat it like a board meeting, not a casual checkup. Review objective data only. No tweaking based on a bad week or an exciting run. That emotional discipline is what separates traders who optimize well from those who just fiddle endlessly.

Why algorithm optimization is the real edge, beyond technology

Here is the uncomfortable truth that most algorithmic trading content skips: the technology is not your edge. Thousands of traders are using the same MT4, the same indicators, and similar EAs. The real differentiator is whether you have built a systematic, unbiased process for continuous improvement.

The traders who consistently outperform over years are not the ones with the most sophisticated algorithms. They are the ones who stick to an optimization schedule even when their account is doing well, who resist the urge to overtrade or over-tune after a losing streak, and who treat their trading system like a business asset that requires regular maintenance rather than a magic box that runs itself.

Most traders abandon their algorithms at exactly the wrong moment, usually right after a drawdown that proper optimization would have caught months earlier. They also over-tinker after a winning streak, chasing more profit and unknowingly introducing overfitting.

“Consistent optimization is not about making the algorithm smarter. It is about making the trader more disciplined.”

The best gold trading systems are not necessarily the most complex. They are the ones that have been rigorously tested, honestly validated, and maintained by traders who understand that edge comes from process, not from technology alone. Your algorithm reflects your discipline. Optimize accordingly.

Unlock your trading edge with proven tools and resources

You now have the framework. The next step is putting it to work with the right tools built specifically for Forex and gold trading automation.

At FxShop24, we develop and curate EAs, trading robots, and automation systems built with optimization in mind from the ground up. Our AI Trading Bot V3.0 is engineered for adaptive performance across both trending and volatile gold and Forex markets. If you are newer to automation or want to understand the foundational case for trading with expert advisors, we have resources to walk you through every stage. From selecting the right EA to setting up your quarterly optimization reviews, FxShop24 gives you the infrastructure to trade systematically and grow with confidence.

Frequently asked questions

What is the main risk when optimizing trading algorithms?

The main risk is overfitting, where an algorithm is too closely tailored to past data and fails to perform in live trading conditions.

How often should I optimize my trading algorithms?

Review and optimize your algorithms at least quarterly. Periodic quarterly reviews without emotional tweaks keep performance stable while avoiding overcorrection between cycles.

Does algorithm optimization work for both Forex and gold trading?

Yes. Both markets benefit from regular optimization. Mechanical systems for gold trading eliminate human biases and ensure consistent execution, and the same principles apply to Forex pairs.

What advanced techniques can improve optimization results?

Monte Carlo simulation, out-of-sample testing, and adaptive retraining with machine learning are the most effective techniques for improving algorithm robustness and long-term effectiveness.