16

May

The role of testing in trading: a guide for forex traders

TL;DR:

- Testing in trading is essential for verifying a strategy’s real edge, not just its theoretical potential.

- Using backtesting, forward testing, and walk-forward analysis together provides a comprehensive validation process before risking live capital.

Most retail forex traders skip straight to live markets with nothing but a chart pattern and confidence. The role of testing in trading is not a box to check before deployment — it is the entire process by which you find out whether your strategy has a real edge or just looks good on paper. Studies on retail trading performance consistently show that the majority of losing traders never conducted structured testing before risking real capital. Backtesting, forward testing, and walk-forward analysis exist precisely to close the gap between a strategy that appears profitable and one that actually performs under real conditions.

Table of Contents

- Understanding the basics of testing in trading

- How backtesting shapes trading strategy development

- Bridging theory and practice with forward testing

- Using walk-forward analysis to detect overfitting

- Accounting for real-world trading costs and execution risks

- The overlooked truth about testing and retail traders

- Explore expert-tested automated trading systems and tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Testing methods explained | Backtesting, forward testing, and walk-forward analysis each serve unique roles in validating trading strategies. |

| Realistic assumptions | Incorporating realistic spread, slippage, and commissions is critical for accurate test results. |

| Forward testing limits | Forward testing requires 100+ trades and time, but offers stronger validation than backtesting alone. |

| Overfitting risks | Walk-forward analysis helps identify overfitting to avoid false confidence in optimized strategies. |

| Testing enhances confidence | Proper testing supports evidence-based decisions and risk management for better trading outcomes. |

Understanding the basics of testing in trading

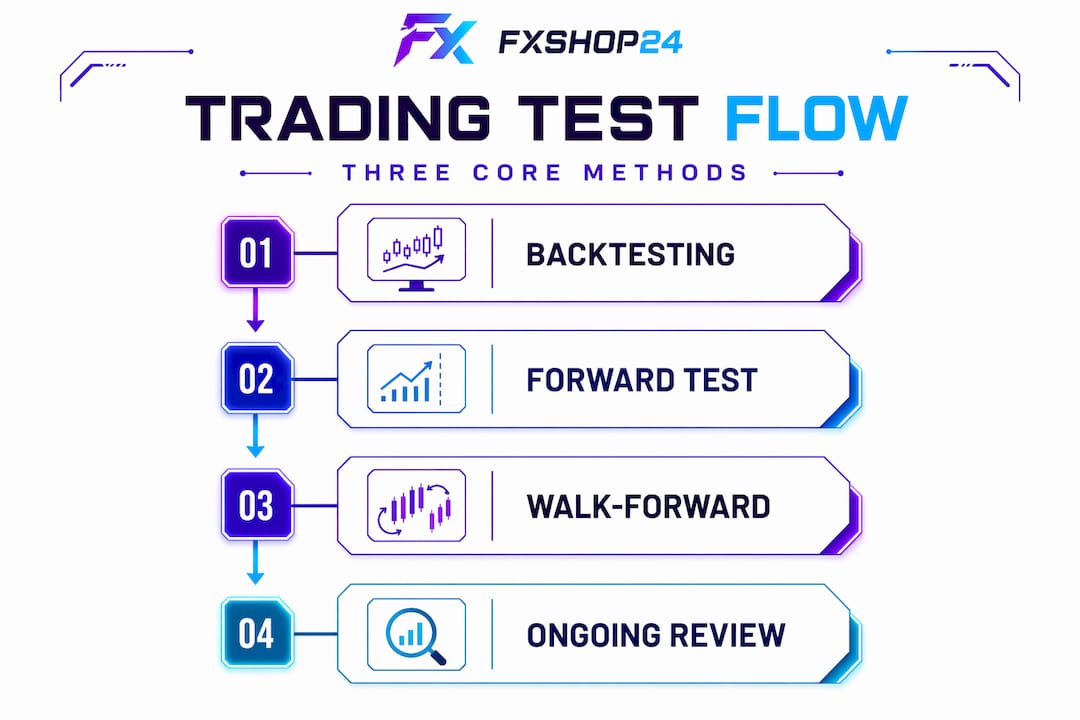

Three core methodologies form the foundation of any serious trading system testing process: backtesting, forward testing, and walk-forward analysis. Each answers a different question, and skipping any one of them leaves a blind spot in your evaluation.

Backtesting simulates your strategy against historical price data to measure how it would have performed in the past. It is the starting point for nearly every professional and automated trader. However, backtesting strategies historically can be prone to overfitting and optimism bias, meaning results can look spectacular on past data and fall apart on live markets. Think of backtesting as the interview, not the job.

Forward testing takes your strategy into a demo account where it encounters live price feeds, real spreads, and genuine market noise. Forward testing on real-time data validates robustness beyond historical periods, confirming whether the edge you identified in backtesting survives actual market behavior. This step is what separates traders who are overconfident in simulated results from those who deploy capital wisely.

Walk-forward analysis (WFA) is the most rigorous of the three. It splits your data into training periods and out-of-sample validation windows, repeatedly testing whether optimized parameters hold up when they encounter data they were never trained on. This is the standard approach for validating expert advisors (EAs), and it is covered in detail when evaluating trading robots for real-world use.

Here is a quick breakdown of what each method tests:

- Backtesting: Historical performance, statistical edge, drawdown profiles

- Forward testing: Real execution quality, psychological durability, spread and slippage behavior

- Walk-forward analysis: Parameter stability, overfitting detection, adaptive durability

- Combined use: A complete, layered validation picture before any live capital is risked

No single method is sufficient on its own. Used together, they give you the most honest picture possible of how a strategy will behave when real money is on the line.

How backtesting shapes trading strategy development

Backtesting is where trading strategy analysis begins, but doing it poorly is almost worse than not doing it at all. The results of a poorly constructed backtest can give you false confidence that destroys accounts.

The first requirement is data quality. High modeling quality above 90% and sufficient trade counts of 100 or more are critical to meaningful backtests. If you are testing an EA in MT4 or MT5 with low-quality tick data, the results are essentially fiction. You need M1 or tick-level data with accurate spread modeling to get anything reliable.

The second requirement is realistic cost modeling. Ignoring spreads, slippage, and commissions leads to unrealistic performance, and XAUUSD spreads range from $0.30 to $1.50 normally. For a scalping strategy on gold, this difference alone can flip a profitable backtest into a losing system. When you backtest an EA on MT5, always input your broker’s real spread and add slippage buffer, especially around news events.

Pro Tip: Run your backtest twice — once with default spreads and once with spreads doubled. If the strategy collapses when spreads widen slightly, it does not have a real edge. It only works in ideal conditions that rarely exist in live trading.

Here are the key metrics to track during every backtest:

- Profit factor: Aim for 1.2 or higher; below 1.0 is a losing strategy by definition

- Max drawdown: Keep it under 50%; anything higher is unlikely to survive live conditions psychologically or financially

- Expectancy: Average expected profit per trade, accounting for wins and losses

- Trade distribution: Look for consistency across months and market conditions, not clustered wins

| Metric | Minimum acceptable | Strong result |

|---|---|---|

| Profit factor | 1.2 | 1.6 and above |

| Max drawdown | Below 50% | Below 20% |

| Trade count | 100 trades | 300 and above |

| Modeling quality | 90% | 99% |

| Win rate (context-dependent) | Varies by R:R | Consistent across periods |

Understanding risk management in trading is inseparable from interpreting these metrics correctly. A high win rate paired with poor risk-to-reward ratios is one of the most common and most dangerous false signals a backtest can produce.

Bridging theory and practice with forward testing

After a backtest delivers promising numbers, many traders skip straight to live accounts. This is a serious mistake. Forward testing is the bridge that turns theoretical results into real-world confidence.

Here is a structured approach to forward testing effectively:

- Set up a demo account that mirrors your intended live trading conditions, including account size, leverage, and instrument spreads from your actual broker.

- Run the strategy without modification for a defined period. Any adjustment mid-test invalidates the results.

- Track every trade manually, including entry time, exit time, actual fill price versus expected price, and spread at execution.

- Compare forward results against your backtest benchmark to identify whether the edge is holding or degrading.

- Do not stop early due to a losing streak. Forward testing needs 100 to 200 trades across multiple market conditions for statistical significance.

What forward testing reveals that backtesting simply cannot is execution reality. Forward tests expose slippage and spread effects that are essential for transitioning to live forex and gold trading. In volatile XAUUSD sessions, a one-pip fill delay can mean the difference between a profitable trade and a stop-out.

Pro Tip: Keep a written journal during forward testing. Not just the numbers — note your emotional state, the temptation to intervene manually, and the moments you wanted to override the system. This data tells you as much about your psychological readiness as it does about the strategy’s performance.

For traders running automated systems, learning the process of boosting backtest results into forward-test-ready setups can significantly shorten the development cycle without sacrificing rigor.

Using walk-forward analysis to detect overfitting

Overfitting is the silent killer of trading strategies. A system that has been tuned to fit past data too precisely performs beautifully in backtests and fails immediately on live markets. Walk-forward analysis (WFA) is designed specifically to expose this problem.

Here is how WFA works in practice. You take your full dataset and divide it into multiple sequential windows. Each window has an in-sample (IS) portion used for optimization and an out-of-sample (OOS) portion used for validation. You optimize parameters on the IS data, then test those exact parameters on the OOS data. You repeat this across all windows and measure consistency. Walk-forward analysis splits data into in-sample optimization and out-of-sample validation to reveal overfitting in ways a simple backtest never can.

The critical insight is what happens in the OOS segments. If your strategy performs consistently well across all out-of-sample windows, you likely have a real edge. If it collapses or produces erratic results in the OOS segments, you have a curve-fitted system that has memorized the past rather than captured a genuine market behavior pattern.

| Testing method | Overfitting detection | Execution realism | Statistical rigor |

|---|---|---|---|

| Basic backtesting | Low | Low | Medium |

| Forward testing | Medium | High | Medium |

| Walk-forward analysis | High | Low | High |

| Combined approach | Very high | Very high | Very high |

MT5 includes a built-in forward optimization feature that simplifies early WFA assessments, making it accessible without third-party tools. For traders serious about validating gold and forex EAs, incorporating WFA into your forex gold trading workflow is not optional — it is what separates a testable system from a gamble with extra steps.

Accounting for real-world trading costs and execution risks

Testing without accurate cost modeling is like stress-testing a car with no weight in it. The results will always look better than reality.

The costs that most traders underestimate are:

- Spreads: XAUUSD spreads vary from $0.30 in calm conditions to $1.50 or more during news events. A strategy that targets 10-pip gains gets destroyed by a 5-pip spread spike.

- Slippage: Stop orders and market entries during fast-moving conditions fill at worse prices than expected, reducing your actual expectancy on every trade.

- Commissions: Counted on both sides of every trade, commissions erode scalping strategies fastest. Model them exactly as your broker charges.

- Swaps (overnight financing): For positions held overnight, swap charges accumulate and must be modeled across your expected holding period.

Ignoring trading costs can turn profitable backtests into losing live trades, especially for gold with spreads of $0.30 to $1.50. This is not a minor adjustment — for high-frequency strategies, it changes the entire performance profile. Realistic spread and slippage assumptions during news and volatile events are essential in any serious testing procedure.

Pro Tip: Deliberately stress-test your strategy by setting spreads to three times your broker’s average during backtesting. Any edge that survives that stress is genuinely robust. If the results disappear, the strategy was only working because of artificially favorable conditions.

Sound risk management in automated trading requires that these costs are not afterthoughts — they are built into position sizing, stop placement, and profit target calculations from the very beginning.

The overlooked truth about testing and retail traders

Here is something the testing guides rarely say plainly: a great backtest is not an asset. It is a liability if you trust it too much.

Retail traders consistently fall into a specific trap. They run a backtest, see a beautiful equity curve, and interpret it as a promise. They deploy capital immediately. When the strategy underperforms in live conditions — which it almost always does to some degree — they blame the broker, the market, or the software. The real issue is that they never understood what the backtest was actually telling them.

Backtesting provides evidence, not proof, and dramatically improves your odds but does not guarantee success. Read that carefully. Evidence. Not certainty. The role of backtesting in trading is to raise your confidence incrementally through layers of validation, not to hand you a finished product.

The traders who succeed with systematic strategies — whether manual or automated — treat testing as an ongoing process, not a one-time gate. They re-test after market regime changes. They re-test when their broker changes spread structures. They question every assumption in their model. This skeptical, iterative mindset is what filters false edges from real ones.

There is also a psychological dimension that testing cannot fully address. You can forward-test a strategy for 200 trades and still freeze when you face three consecutive losses in a live account with meaningful capital at risk. Testing builds intellectual confidence. The emotional resilience to execute through drawdowns is built separately through experience and discipline. Any approach to evaluating trading robots or manual strategies must account for both the quantitative and the psychological readiness of the trader behind the system.

Explore expert-tested automated trading systems and tools

Understanding testing methodology is the first step. The second is applying it to systems that have already been built with these standards in mind.

At FxShop24, every expert advisor in our catalog has gone through structured backtesting and forward testing across forex and XAUUSD markets before it reaches you. You can browse our range of automated trading systems for MT4 and MT5, each with documented test results and risk profiles. If you want to sharpen your own evaluation skills, our guide on evaluating trading robots walks you through exactly what to look for. And for traders ready to stress-test systems themselves, our detailed walkthrough on backtesting trading robots covers the entire process from data setup to interpreting results.

Frequently asked questions

What is the main difference between backtesting and forward testing?

Backtesting evaluates a strategy using historical data, while forward testing applies the strategy on real-time or demo data going forward — forward testing uses current prices as they develop, not historical prices that already exist, making it a true future-facing validation step.

How many trades should a forward test include to be statistically meaningful?

A forward test should include at least 100 to 200 trades across multiple market conditions. Fewer than 100 trades across different market conditions does not produce statistically meaningful results and risks false conclusions based on luck rather than edge.

Why is it important to include realistic spreads and slippage in backtests?

Including realistic spreads and slippage prevents overestimating profits and ensures backtests better reflect live trading conditions. Profitable backtests can become losing live trades when cost modeling is ignored, especially for instruments like gold where spreads are significant.

What does walk-forward analysis help detect in trading strategies?

Walk-forward analysis detects overfitting by testing whether optimized parameters on past data remain effective on unseen future segments. WFA reveals overfitting that a standard backtest will miss entirely, ensuring the strategy is capturing real market behavior rather than memorizing historical noise.

Can backtesting guarantee trading profits?

No. Backtesting provides evidence, not proof, and while it dramatically improves your odds of finding a real edge, live conditions, psychological factors, and changing market regimes all affect outcomes in ways no historical simulation can fully capture.