9

Mar

Master risk management in automated trading MT4 MT5

Automated trading promises effortless profits, but without proper risk management, it can drain your account faster than manual trading ever could. Most traders using MT4 and MT5 Expert Advisors fail because they underestimate the unique risks of algorithmic systems. This guide reveals the essential risk management techniques you need to protect your capital and achieve consistent returns with automated forex trading.

Table of Contents

- Introduction To Automated Trading Risk Management

- Core Risk Metrics And Their Interpretation

- Common Misconceptions About Risk In Automated Trading

- Key Risk Management Techniques Specific To MT4/MT5

- Robust Testing And Validation Of Automated Strategies

- How Fxshop24 Supports Your Automated Trading Risk Management

- FAQ

Key takeaways

| Point | Details | |-------|---------|| | Dynamic risk controls outperform static approaches | Automated systems require adaptive stop losses, position sizing, and drawdown limits that respond to changing market conditions. | | Key metrics reveal true strategy health | Max drawdown and Sharpe ratio expose hidden risks that win rate alone cannot show, preventing catastrophic losses. | | Testing beyond backtests prevents surprises | Forward testing and Monte Carlo simulations catch overfitting and reveal realistic performance expectations before live deployment. | | Platform-specific techniques maximize protection | MT4 and MT5 offer unique tools for news filters, dynamic stops, and automated trade pauses that manual traders cannot replicate. |

Introduction to automated trading risk management

Automated trading on MT4 and MT5 introduces risks that manual traders rarely face. Algorithmic errors, platform latency, and sudden market volatility can trigger losses before you even notice a problem. Unlike manual trading where you can pause and reassess, automated forex trades on MT4 and MT5 execute without human intervention, making code integrity and system monitoring critical.

The difference between manual and automated risk is fundamental. Manual traders control every decision in real time, adapting to market shifts intuitively. Automated systems depend entirely on preprogrammed logic, which can fail spectacularly when market conditions change. A single coding error or unexpected news event can wipe out weeks of gains in minutes.

Poor risk management in automated trading leads to unexpected drawdowns that destroy accounts. Without proper controls, a winning EA can turn into a capital destroyer during volatile periods or system failures. Understanding MT4 vs MT5 comparison helps you choose the right platform features for your risk management needs.

MT4 and MT5 platforms offer specific tools for risk control that traders must learn to leverage. Built-in functions for position sizing, stop loss automation, and trade monitoring create the foundation for effective risk management. However, these tools only work when properly configured and continuously monitored.

Core risk metrics and their interpretation

Max drawdown measures the largest peak to trough decline in account equity, revealing the worst-case scenario your strategy has experienced. This metric matters more than profit percentage because it shows how much capital you risk losing during difficult market periods. A strategy with 200% returns but 80% drawdown will likely destroy your account before you see those gains.

Sharpe ratio divides excess returns by volatility, providing a risk-adjusted performance measurement that separates lucky streaks from genuine edge. A Sharpe ratio above 1.0 indicates acceptable risk-adjusted returns, while values above 2.0 suggest exceptional performance. This metric helps you compare strategies with different volatility profiles on equal footing.

Win rate alone misleads traders into false confidence. A 90% win rate means nothing if the 10% of losing trades wipe out all gains from winners. Algorithmic trading strategies must balance win rate with average win size, average loss size, and maximum consecutive losses to assess true profitability.

Pro Tip: Always compare metrics from both backtests and forward tests to avoid overconfidence in historical performance that may not repeat in live markets.

| Metric | Backtest Value | Forward Test Value | Interpretation |

|---|---|---|---|

| Max Drawdown | 15% | 23% | Higher live drawdown suggests overfitting |

| Sharpe Ratio | 2.1 | 1.4 | Still acceptable but lower than historical |

| Win Rate | 72% | 68% | Consistent performance across test types |

| Profit Factor | 2.8 | 2.1 | Reduced but viable live performance |

Live drawdowns can exceed backtest max drawdowns by up to 50% due to overfitting and changing market conditions. This discrepancy explains why traders often experience shock when their thoroughly backtested EA performs worse in real trading. The forward test column reveals the more realistic expectations you should set for live performance.

Common misconceptions about risk in automated trading

Myth 1: Higher leverage guarantees higher profits. In reality, excessive leverage amplifies losses just as much as gains, increasing the probability of account ruin without strict stop losses. Most professional traders use leverage conservatively, typically 1:10 or less, to preserve capital during unexpected market moves.

Myth 2: Backtests guarantee live results. Historical performance ignores overfitting, where strategies optimize for past data but fail on new market conditions. Without forward testing and out-of-sample validation, you are essentially driving by looking only in the rearview mirror.

Myth 3: Static stop losses suffice for all market conditions. Fixed stop distances fail during high volatility periods when normal price swings trigger premature exits, or during low volatility when stops sit too wide and allow excessive losses. Optimizing automated trading on MT4 and MT5 requires dynamic risk controls that adapt to current market behavior.

Backtests often overfit past data; live trading performance may show 20-50% greater drawdowns than backtests suggest, making forward testing essential.

These misconceptions cause common trading failures because they create false confidence. Traders launch EAs with inflated expectations, inadequate capital buffers, and no contingency plans for when reality diverges from backtest results. The gap between expectation and reality triggers emotional decisions that compound losses.

Understanding these myths helps you build more realistic risk models. When you expect larger drawdowns, adapt stops to volatility, and use conservative leverage, you create sustainable automated trading systems that survive market turbulence.

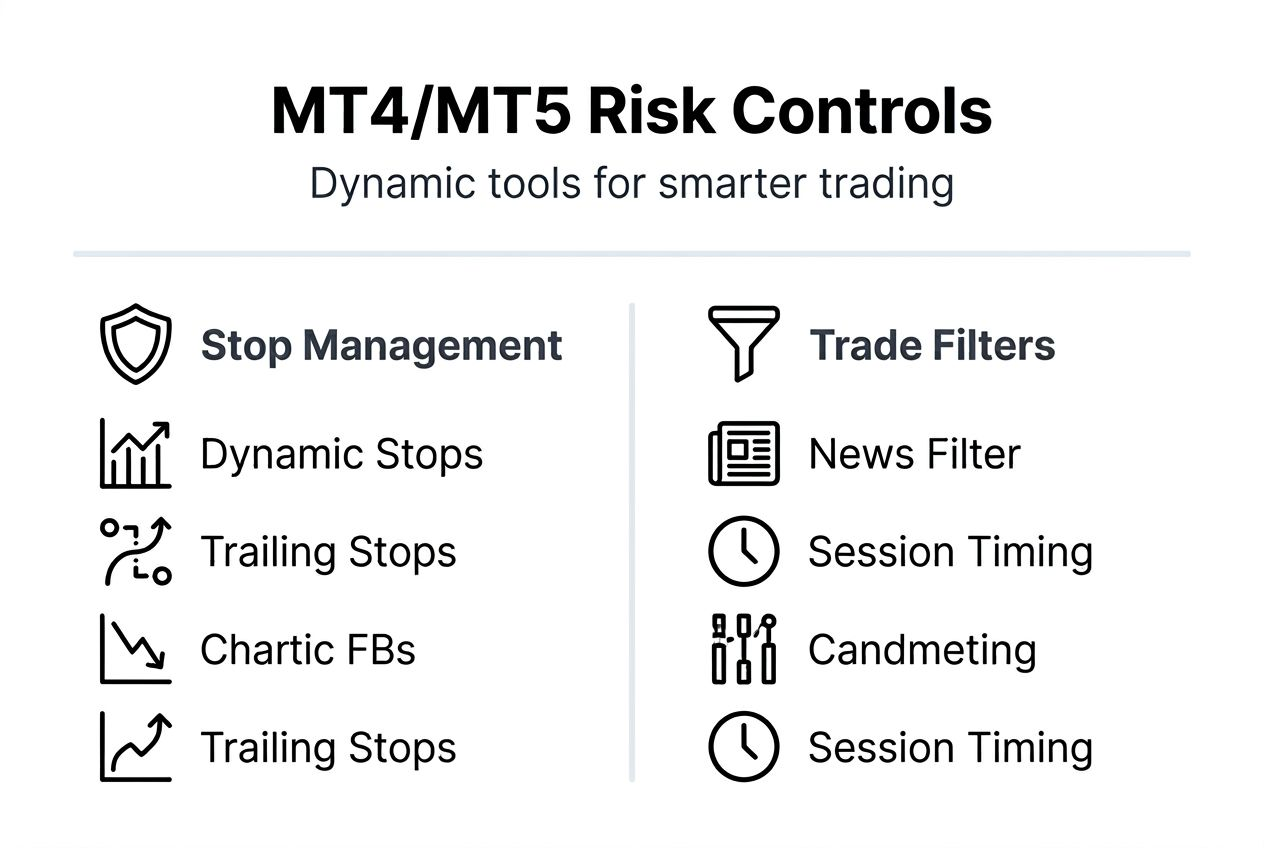

Key risk management techniques specific to MT4/MT5

Dynamic stop loss and take profit settings adjust to current market volatility, providing tighter protection during calm periods and wider allowances during volatile sessions. Static stops fail because markets constantly change character, making fixed distances either too tight or too loose.

| Feature | Static Stops | Dynamic Stops |

|---|---|---|

| Adapts to volatility | No | Yes |

| ATR-based calculation | No | Yes |

| Reduces whipsaws | Limited | Excellent |

| Programming complexity | Simple | Moderate |

Economic calendar news filters pause or reduce trading during high-impact events like NFP, FOMC, or GDP releases. Coding these filters into your EA prevents catastrophic losses from unpredictable price spikes that often accompany major announcements. Essential MT4 and MT5 trading tools include news indicator plugins that integrate seamlessly with EA logic.

Drawdown control features include maximum drawdown limits that automatically pause trading when equity declines beyond acceptable thresholds. Implementing automated trade pauses protects capital during losing streaks, preventing the spiral where losses compound as traders chase recovery.

Steps to implement these controls in EA programming:

- Calculate current ATR value and multiply by a factor (typically 2-3) to set dynamic stop distance

- Add news filter function that checks upcoming events within specified time window

- Create equity monitoring loop that compares current drawdown to maximum threshold

- Program automatic trade pause when drawdown limit is breached

- Set recovery conditions that resume trading only after equity recovers to safe levels

Pro Tip: Align stop levels dynamically to market volatility by using ATR or standard deviation calculations, reducing premature exits during normal price fluctuations while maintaining protection during genuine reversals.

Robust testing and validation of automated strategies

Out-of-sample backtesting splits historical data into training and validation sets, ensuring your strategy performs on unseen data rather than just memorizing past patterns. This technique catches overfitting early, before you risk real capital on a curve-fitted system.

Walk-forward optimization continuously re-optimizes strategies on rolling time windows, adapting parameters as market conditions evolve. This approach acknowledges that optimal settings change over time, preventing the performance decay that plagues static strategies.

Monte Carlo simulations improve risk metric confidence intervals by modeling slippage, latency, and varying conditions, widening drawdown estimates by around 15%. Running thousands of simulated trades with randomized order and execution conditions reveals the full range of potential outcomes, not just the single path shown in standard backtests.

Stepwise testing approach summary:

- Split data into 70% training, 30% validation sets before any optimization

- Optimize on training data only, then test on validation set without changes

- Run Monte Carlo analysis with at least 1,000 simulations including realistic slippage

- Perform walk-forward analysis over multiple time periods to test adaptability

- Conduct forward testing on demo account for minimum 3 months before live deployment

The most common pitfall is overfitting, where excessive parameter tweaking creates strategies that perform brilliantly on historical data but fail immediately in live markets. Automated trading strategy examples demonstrate how simpler strategies with fewer parameters often outperform complex, heavily optimized systems.

Robust testing methodologies require patience and discipline. Traders eager to launch profitable EAs skip validation steps, learning expensive lessons when live results disappoint. Investing time in thorough testing saves far more capital than rushing to market.

How fxshop24 supports your automated trading risk management

After mastering risk management principles, you need reliable tools and systems to implement these strategies effectively. Fxshop24 offers a curated selection of automated trading systems for MT4 and MT5 designed with robust risk controls built in, saving you months of development time.

Our guide to optimizing trading robots walks you through advanced techniques for improving EA performance while maintaining strict risk parameters. Combined with our trading robot setup guide for MetaTrader, you gain comprehensive support from installation through optimization.

These resources complement the risk management strategies covered in this article, helping you implement dynamic stops, drawdown controls, and robust testing protocols. Whether you are building custom EAs or using pre-made systems, fxshop24 provides the tools and knowledge to trade automated systems safely and profitably.

FAQ

What key risk metrics should I monitor in automated trading?

Max drawdown and Sharpe ratio are essential for assessing risk and performance. Max drawdown shows your worst-case capital decline, while Sharpe ratio measures risk-adjusted returns. Monitoring win rate alongside risk exposure gives a fuller picture than any single metric alone.

How can I reduce unexpected large losses in live EA trading?

Use forward and stress testing to validate EAs beyond backtests, exposing weaknesses before risking real capital. Implement dynamic stop losses and automated drawdown limits in live trading. These controls pause trading during losing streaks, preventing catastrophic equity destruction.

What are common mistakes in automated trading risk management?

Overreliance on backtests without forward validation creates false confidence in untested strategies. Ignoring market volatility in stop loss settings leads to either premature exits or excessive losses. Neglecting real-time monitoring and automated trade pause functions allows problems to compound unchecked, turning manageable drawdowns into account disasters.

Why do live results differ from backtest performance?

Backtests optimize on historical data, creating strategies that may overfit past patterns without generalizing to new conditions. Slippage, latency, and spread variations in live trading reduce profitability compared to simulated fills. Market regime changes also shift strategy effectiveness, making historical performance an imperfect predictor of future results.

How often should I review and adjust my EA risk parameters?

Review risk parameters monthly or after significant market regime changes like volatility spikes or trending to ranging shifts. Walk-forward optimization helps identify when parameters need adjustment versus temporary underperformance. Avoid over-tweaking based on short-term results, which often leads to optimization bias and degraded performance.