2

May

Understand Forex Liquidity to Boost Automated Trading

TL;DR:

- Forex market liquidity influences spreads, slippage, and order execution, impacting automated trading performance.

- Retail traders face aggregated liquidity with delays; prop firms access deeper, faster, and more stable liquidity.

- High liquidity environments enhance quant strategy profitability, challenging the myth that more trades reduce profits.

The forex market processes a staggering $9.5 trillion in daily turnover as of April 2025, making it the most liquid financial market on earth. Yet most traders running Expert Advisors (EAs) on MT4 and MT5 treat liquidity as background noise rather than a core variable in their strategy design. That is a costly mistake. Liquidity is not a fixed, uniform force you can ignore. It shapes your fills, your slippage, your drawdown, and ultimately your profitability. This guide cuts through the confusion, explains the real mechanics behind forex liquidity, and shows you exactly how to leverage them inside your automated trading setup.

Table of Contents

- What is forex market liquidity and why does it matter?

- How liquidity dynamics differ for retail traders and prop firms

- Turnover, liquidity, and profitability: Myths vs. reality

- How to adapt automated trading strategies for liquidity conditions

- A fresh perspective: Why liquidity management is the real secret to automated trading success

- Level up your automation with the right tools

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Liquidity shapes execution | True forex liquidity directly affects order fills, slippage, and profitability for both retail and prop traders. |

| Retail vs. prop access | Prop firms benefit from deeper, faster liquidity access than most retail setups, impacting automated results. |

| High turnover’s upside | Recent studies show higher liquidity can boost returns for machine-driven and algorithmic trading strategies. |

| Adapt EAs for conditions | Tuning automated strategies for real-world liquidity improves consistency and win rate. |

What is forex market liquidity and why does it matter?

Liquidity is simply the ability to buy or sell an asset quickly at a stable, predictable price. In forex, high liquidity means tight bid-ask spreads, minimal price slippage, and fast order execution. Low liquidity means the opposite: wider spreads, price gaps, and fills that land nowhere near your target entry.

Here is what most retail traders miss. The liquidity you see inside your MT4 or MT5 terminal is not the full picture. Your broker aggregates prices from multiple liquidity providers, including banks, hedge funds, and electronic communication networks (ECNs). What you see is a filtered, packaged version of a much deeper interbank market. The displayed spread and order depth do not always reflect true market conditions in real time.

Why does this matter for automation? Because your EA makes decisions based on the data it receives. If that data is lagged, aggregated, or compressed by your broker’s infrastructure, your EA could trigger trades at prices that are already stale. For scalping robots or high-frequency strategies, even a 10-millisecond lag can flip a profitable signal into a losing fill.

Key reasons liquidity shapes automated performance:

- Spread behavior: Liquidity thins during off-hours (Sydney open, Friday close), causing spreads to widen. An EA that does not account for this may trigger entries with a built-in loss from the start.

- Slippage tolerance: High-volume periods like the London-New York overlap deliver tighter fills. Your EA’s slippage parameters should reflect this reality.

- Order depth: The visible order book on retail platforms is shallow compared to institutional depth. A large position for a retail trader can still move price in thinly traded exotic pairs.

- Fill speed: Broker infrastructure and server location directly affect how quickly your EA’s order reaches the market and gets executed.

“The forex market’s daily turnover hit $9.5 trillion in April 2025, a 27% jump from $7.5 trillion in 2022, confirming it as the world’s most liquid market. But scale alone does not guarantee smooth execution for every participant.”

Understanding these mechanics is not just academic. It is the difference between an EA that performs consistently on live accounts and one that looks great in backtesting but bleeds capital in real market conditions.

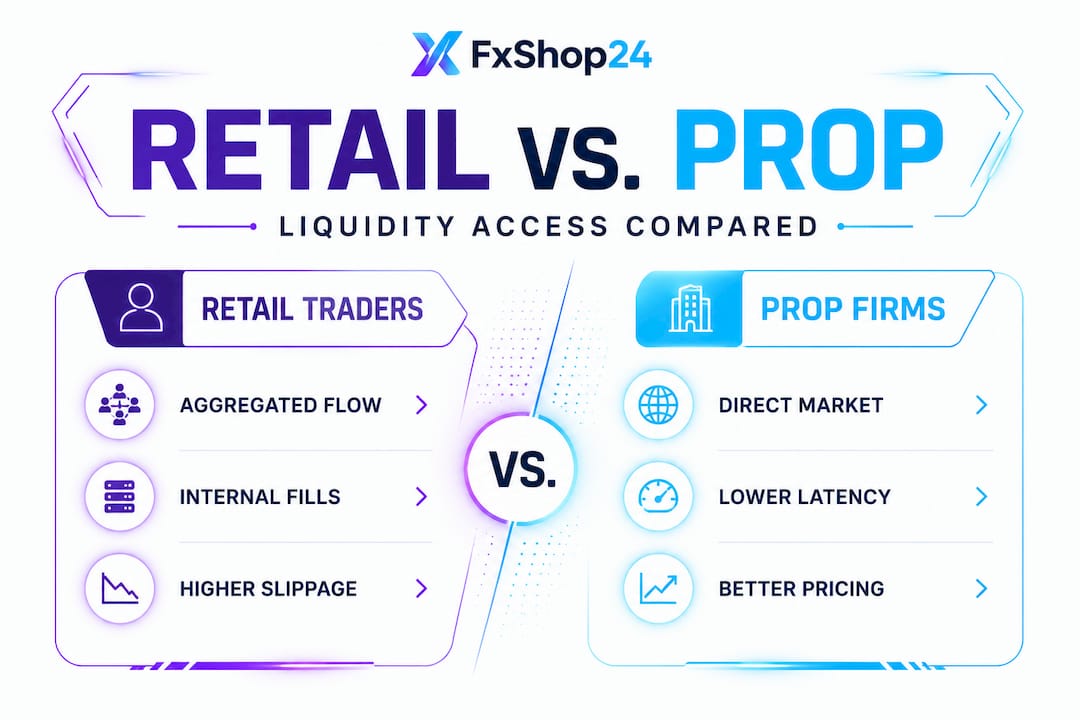

How liquidity dynamics differ for retail traders and prop firms

Understanding liquidity basics sets the stage for a more important question: does everyone in the forex market experience it the same way? Absolutely not.

Retail traders using standard MT4 or MT5 accounts access what brokers call aggregated liquidity. Multiple liquidity providers feed prices into the broker’s system, which then offers a single blended quote to the trader. This works fine for most strategies, but it introduces layers of separation between you and the actual interbank market. Liquidity risk at this level includes sudden spread widening during news events, partial fills on larger orders, and re-quotes during fast markets.

Proprietary trading firms operate on a completely different level of access. Many prop firms co-locate their servers at Equinix data centers, placing their execution infrastructure physically closer to exchange matching engines. This dramatically reduces latency. Where a retail trader might experience 50 to 200 milliseconds of delay between signal and fill, a prop firm operating with co-located infrastructure might achieve sub-millisecond execution. As noted in practitioner research, prop firms access deeper liquidity via institutional partnerships and proximity strategies that retail traders simply cannot replicate at standard account tiers.

Another key structural difference is order internalization. Many retail brokers fill orders internally, meaning your trade never actually reaches the broader market. Instead, the broker absorbs it using its own book or matches you against another client. This is not inherently bad. It can reduce market impact for smaller orders and sometimes produces faster fills. But it also means the liquidity you experience is artificial in a sense, managed by the broker rather than the open market.

Understanding prop trading advantages can help retail traders identify areas where they can close the gap. Choosing an ECN broker, using a VPS server in a major financial hub, or trading during peak liquidity windows are all steps retail traders can take to improve their execution environment.

Pro Tip: If you are running EAs on a standard retail account, always check whether your broker is STP (Straight Through Processing) or market-maker. STP brokers route orders directly to liquidity providers, giving your EA more realistic fills. Market-maker brokers internalize most orders, which changes how your EA’s slippage settings should be calibrated.

| Factor | Retail traders | Prop firm traders |

|---|---|---|

| Liquidity source | Aggregated, broker-filtered | Institutional, direct or near-direct |

| Execution speed | 50 to 200ms typical | Sub-10ms with co-location |

| Order book depth | Shallow, broker-managed | Deeper, multi-tier access |

| Spread during volatility | Widens significantly | More stable, tiered pricing |

| Infrastructure options | Standard VPS | Equinix co-location |

| Order internalization | Common | Reduced or eliminated |

What is prop trading explains the structural setup in more detail. Even if you are currently trading retail, understanding the prop model helps you benchmark your own execution quality against what is actually possible.

Turnover, liquidity, and profitability: Myths vs. reality

With those structural differences established, it is time to confront a stubborn myth that trips up many EA developers and traders alike.

Traditional trading wisdom, especially from discretionary and fundamental traders, often argues that high turnover is the enemy of profitability. The logic goes: more trades mean more commissions, more slippage, and lower net returns. This made sense in an era of manual trading with fixed spreads and high brokerage fees. But for automated trading strategies, the calculation changes completely.

Recent quantitative research tells a very different story. A dual-market study examining machine-driven strategies found that higher liquidity boosts quant returns, with net returns reaching 107% in high-turnover, high-liquidity environments. The reason is straightforward: algorithms thrive on consistency. When liquidity is deep and stable, an EA can execute its strategy repeatedly with minimal friction. Each fill is close to the intended price, slippage is predictable, and the strategy’s edge compounds cleanly over hundreds or thousands of trades.

“Traditional theory links high turnover to lower returns, but machine-driven quant trading flips this entirely. Higher liquidity and turnover boosted net returns by 107% in a recent dual-market study, proving that automation fundamentally changes the liquidity-profitability relationship.”

Key myths debunked:

- Myth: More trades always mean lower profits. Reality: For well-calibrated EAs in liquid markets, higher trade frequency exploits more opportunities with minimal additional friction.

- Myth: Low-volume periods create better setups. Reality: Low liquidity periods increase slippage and spread costs, often destroying any technical edge your EA identified.

- Myth: Backtests reflect real execution. Reality: Most backtesting engines use fixed spreads and ideal fill assumptions, masking the liquidity-driven costs your EA will actually face live.

- Myth: Slippage is random. Reality: Slippage is highly correlated with session timing, news events, and broker infrastructure. It is measurable and manageable.

For traders following top trading strategies in 2026, integrating liquidity awareness into strategy design is not optional. It is the difference between a strategy that looks good on paper and one that holds up under live market conditions with real money.

| Trading approach | Liquidity impact | Profitability outcome |

|---|---|---|

| Manual discretionary trading | High turnover hurts via commissions | Often reduced at high frequency |

| Rule-based EA in liquid sessions | Stable spreads, tight fills | Strong edge compounding |

| EA in low-liquidity sessions | Wide spreads, poor fills | Edge eroded or reversed |

| Quant/machine learning EA | Benefits from deep liquidity | Returns amplified with volume |

How to adapt automated trading strategies for liquidity conditions

Knowing the theory is one thing. Putting it into practice inside your MT4 or MT5 EA is another. Here are concrete steps to bring liquidity awareness into your automation workflow.

Build session filters into your EA. Code your robot to only trade during high-liquidity windows. The London session (8am to 12pm GMT) and the London-New York overlap (12pm to 4pm GMT) deliver the tightest spreads and deepest volume in major pairs. For gold (XAUUSD), the New York open is especially critical.

Set dynamic slippage parameters. A fixed slippage allowance ignores the reality that spread conditions change dramatically across the trading day. Set slippage thresholds that widen during news windows and tighten during stable sessions. Many advanced EAs allow slippage as a configurable input.

Test with variable spread data. Most standard MT4/MT5 backtests default to fixed spreads. Use tick data with real spread history, or at minimum run your EA on a demo with live variable spreads before any live deployment. This gives you a far more honest picture of expected fill quality.

Upgrade your infrastructure if execution is a bottleneck. If you are trading a scalping or grid strategy where milliseconds matter, a VPS server located close to your broker’s data center is worth every dollar. Latency in execution can turn a consistent winner into a break-even or losing system.

Monitor broker internalization behavior. Track the difference between your requested price and your actual fill price across a sample of 200 to 500 trades. If your fills consistently land worse than your MT4 terminal’s displayed price, your broker may be internalizing orders in ways that disadvantage your EA’s strategy type.

Research on FX execution algorithms consistently shows that retail traders who understand how their broker processes orders, and who select brokers aligned with their EA’s strategy type, see measurable improvements in net performance. Refer to our guide on mastering order execution for a deeper breakdown of how order routing choices affect your EA’s profitability in practice.

Understanding forex volatility is also essential when adapting automation. Volatility and liquidity are closely linked. Periods of elevated volatility often correspond to sudden drops in effective liquidity, even in major pairs, making your EA’s behavior during high-impact news especially important to monitor and control.

Pro Tip: Add a news filter to your EA that pauses trading 15 minutes before and after major economic releases like NFP, CPI, or central bank decisions. These events create micro-illiquidity spikes even in the most traded pairs, and most EAs are not designed to profit from that kind of chaotic price action.

A fresh perspective: Why liquidity management is the real secret to automated trading success

Most traders shopping for EAs ask the same questions: What is the win rate? What is the maximum drawdown? What is the monthly return? These are reasonable questions, but they miss the deeper driver of consistent performance.

The real differentiator between average EAs and top-performing ones is how they handle strategy design with execution awareness. An EA with a 55% win rate but poor liquidity management will consistently underperform versus an EA with a 50% win rate that executes in optimal liquidity conditions with controlled slippage.

Here is the uncomfortable truth: most EA developers spend 90% of their time refining entry and exit signals and virtually no time thinking about execution quality. Seasoned prop firm traders and institutional quants think about it in reverse. They obsess over fill quality, order routing, latency, and market impact before they even finalize their signal logic. The signal matters less if execution eats your edge on every trade.

For retail traders, this might sound like a problem only institutions can solve. It is not. Simple, practical moves like choosing an ECN broker, trading during liquid sessions, using a well-located VPS, and building slippage tolerance into your EA all shift the odds in your favor. You do not need to be a hedge fund to think like one. You just need to stop treating execution as someone else’s problem.

Liquidity awareness also reframes how you interpret backtest results. An EA that performs brilliantly in a fixed-spread backtest but falls apart live is almost certainly suffering from a liquidity mismatch. The backtest assumed clean, frictionless fills. The live market delivered something messier. Close that gap in your testing methodology and you will immediately get a more honest, useful picture of your EA’s true potential.

Level up your automation with the right tools

Understanding liquidity is the first step. Putting it into practice with the right software is where the real gains happen.

At FxShop24, we build and curate automated systems for MT4 and MT5 specifically designed to perform in real market conditions, not just ideal backtests. Our EAs include built-in session filters, dynamic slippage management, and prop firm-compatible execution logic so your automation adapts to liquidity conditions rather than ignoring them. Whether you are optimizing order execution strategies for a retail account or scaling up with a funded prop account, our tools are tested against live market data. Explore our lineup of trade execution tools and see how smarter automation translates directly into better fills, lower drawdown, and more consistent returns.

Frequently asked questions

What determines forex market liquidity?

Forex liquidity is determined by trading volume, participant diversity, and market infrastructure connecting buyers and sellers worldwide. The BIS April 2025 survey confirmed daily turnover at $9.5 trillion, a 27% increase from 2022.

Does higher forex liquidity always mean better fills for automated trading?

Not always. Retail traders see aggregated liquidity that may still produce slippage or requotes, while institutional proximity via Equinix co-location gives prop firms genuinely superior fill quality.

How can I improve EA performance in low liquidity?

Reduce order sizes, avoid trading during off-peak sessions like the Asian open on exotic pairs, and optimize your VPS location and broker routing to minimize the friction that low-liquidity conditions create.

Why does slippage occur even in high-liquidity periods?

Sudden news events, order queueing at your broker’s server, and internal order internalization can create brief pockets of micro-illiquidity that push fills away from your intended price, even when the broader market is technically deep and liquid.

Recommended

- Automate Or Die: Why Successful Forex Traders Rely On EAs And Robots For Consistent Gains In 2025 | FxShop24 Marketplace

- Master Order Execution In Forex: Strategies For Reliable Fills

- Manual Vs Automated Trading: Optimize Forex And Gold Results

- How To Automate Forex Trades Using MT4 And MT5 Easily

- Automated trading FAQ - Tickerly