6

May

Why diversify trading strategies for smoother results

TL;DR:

- Diversification in trading involves combining strategies with low or negative correlations to smooth equity curves and reduce drawdowns. It requires ongoing correlation analysis and proper risk controls because surface-level diversification can fail during extreme market stress. Building a resilient portfolio demands continuous monitoring, stress-testing, and including uncorrelated, regime-specific systems for long-term survival.

Most traders discover the hard way that a winning expert advisor can fail precisely when markets shift and stress spikes. You trust a system that has performed for months, then a single volatile week erases weeks of gains. The fix most traders reach for is adding more EAs, but diversifying trading strategies is actually about reducing portfolio-level drawdowns by combining approaches that respond to different market regimes and carry low correlation. This article walks you through the real mechanics of diversification, what it actually protects against, and the practical steps to build a portfolio that can survive regime changes without blowing up.

Table of Contents

- Why diversifying trading strategies matters

- How real diversification works: The correlation myth

- Risk controls: Diversification without guardrails can backfire

- Why gold, Forex, and cross-asset portfolios behave differently

- Practical frameworks: How to build robust, diversified trading portfolios

- The uncomfortable truth most traders miss: Even ‘diversified’ portfolios break if you overlook hidden risks

- Take the next step: Build your diversified trading system

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| True diversification priorities | Combining uncorrelated strategies, not just more trades, is the real path to smoother results. |

| Guardrails are essential | Portfolio-wide risk controls prevent runaway losses even with multiple automated systems. |

| Gold’s hedge role varies | Gold’s effectiveness as a diversifier depends on the market regime and changes over time. |

| Correlations shift | Periodically review strategy and asset correlations, as they can spike unexpectedly in stress. |

| Maximize diversification, not just minimize risk | Focusing on strategy diversity leads to portfolios resilient to forecasting errors and market shocks. |

Why diversifying trading strategies matters

The word “diversification” gets overused and under-explained in trading circles. Most retail traders interpret it as spreading money across more EAs or more currency pairs. That’s a partial answer at best and a dangerous assumption at worst.

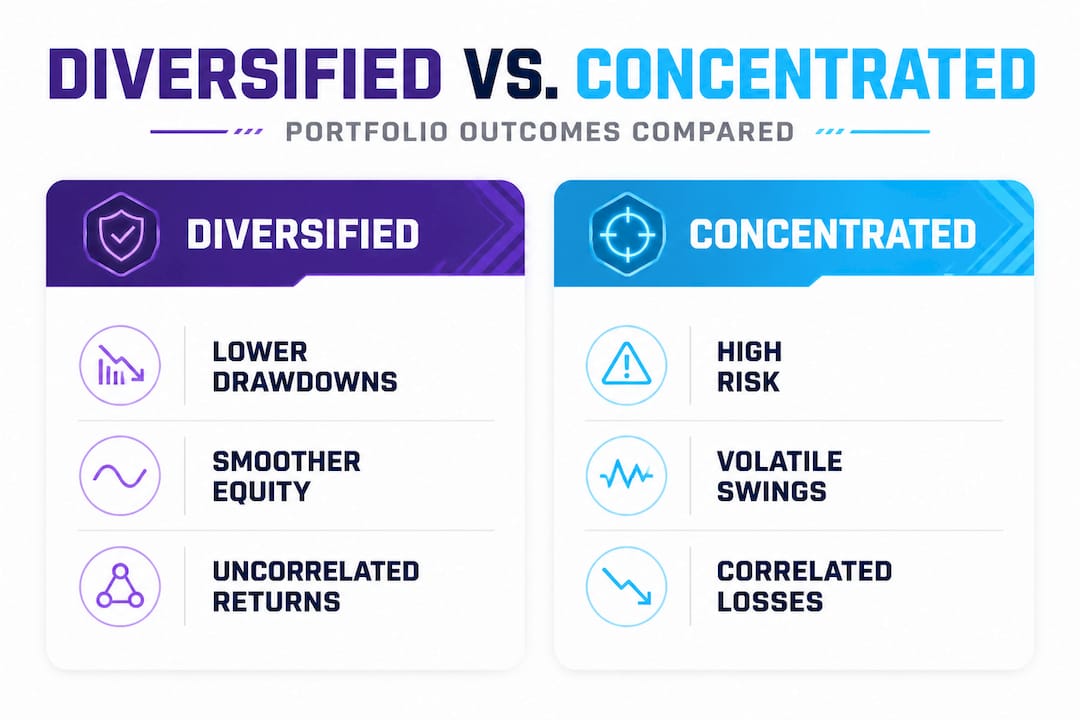

True diversification means building a portfolio where the individual strategies don’t all lose at the same time. It’s about finding systems that seek uncorrelated losses, meaning when one strategy struggles, another is either flat or gaining. That’s what smooths an equity curve over time.

“The goal is not to own more systems, but to own systems that behave differently from one another under the same market conditions.”

Here’s what traders most commonly get wrong:

- Stacking trend-following EAs: Running five trend systems on five currency pairs looks diverse, but they all suffer when markets go sideways or reverse sharply together.

- Ignoring strategy logic: If every EA in your portfolio uses the same entry trigger or indicator family, you have concentrated exposure dressed up as diversification.

- Confusing instrument count with edge variety: More symbols does not mean less risk if the underlying market behavior is similar.

Understanding the system advantages for Forex and Gold is the starting point for building a portfolio that actually holds up. A well-structured mix of mean-reversion, trend-following, and volatility-sensitive strategies gives you a much better chance of staying profitable across different market regimes. Without that, you’re not diversified. You’re just louder.

How real diversification works: The correlation myth

Let’s clear up one of the biggest myths in automated trading: that trading more instruments automatically means lower risk. It does not.

Correlation is the key variable, and it measures how closely two strategies or instruments move together. A correlation close to 1.0 means they move in lockstep. A correlation near 0 means they’re independent. Negative correlation means when one rises, the other tends to fall. Portfolio protection comes from combining low or negatively correlated strategies, not from adding more positions in the same directional environment.

Diversifying across instruments is not automatically diversification if those instruments are highly correlated. Gold and the US dollar index, for example, often move inversely. But during certain macro shocks, like pandemic lockdowns or banking crises, correlations across all assets can spike simultaneously. That’s when a portfolio that felt balanced suddenly becomes vulnerable.

| Portfolio type | Correlation profile | Drawdown during stress | Equity curve smoothness |

|---|---|---|---|

| High correlation | 0.7 to 1.0 | Deep and fast | Volatile, irregular |

| Moderate correlation | 0.3 to 0.6 | Moderate depth | Some smoothing |

| Low/negative correlation | Below 0.3 | Shallow and brief | Consistent, smooth |

Gold’s reputation as a diversifier is real but conditional. It works well during equity selloffs and dollar weakness. However, during liquidity crises, gold can sell off alongside equities because institutions need to raise cash. Treating gold as a guaranteed hedge in your risk management in automated trading framework without checking prevailing correlation is a setup for disappointment.

Pro Tip: Before adding any new EA to your portfolio, run a 90-day correlation check between its returns and your existing strategies. If correlation is above 0.5, adding it gives you very little actual diversification benefit regardless of how different the system appears on paper.

The algorithmic trading benefits of running systematic strategies include the ability to measure these correlations precisely, something a discretionary trader rarely manages to do consistently. That measurability is one of the most underrated advantages of running automated systems.

Risk controls: Diversification without guardrails can backfire

Here’s the part that surprises many experienced traders. Adding more strategies to your account, without portfolio-wide risk controls in place, can actually increase your danger rather than reduce it.

Why? Because each EA runs its own logic and takes its own risk. If five strategies all hit losing streaks simultaneously, which happens in correlated drawdowns, the total loss compounds across all five. Portfolio-wide risk controls, such as account-level drawdown limits, are essential to prevent multiple systems from stacking losses at the same time.

Here’s a straightforward process to set up coordinated risk controls across your EA portfolio:

- Set an account-level daily loss limit: Decide the maximum percentage you’ll allow the entire account to lose in one trading day, typically 1% to 2% for prop firm accounts. When that limit is hit, all EAs stop trading until the next session.

- Assign per-EA position sizing caps: Each EA should be restricted to a maximum lot size proportional to total account equity, not its own isolated logic.

- Implement a maximum drawdown shutdown: Set an absolute drawdown level, such as 5% to 8% total account loss, that automatically suspends all EA activity until you manually review the portfolio.

- Add volatility filters to each EA: High volatility events, like major news releases, should trigger a pause in all systems, not just the ones programmed to avoid news.

- Use a portfolio monitor script: In MT4 or MT5, a custom script or utility EA can track combined open positions, daily P&L, and drawdown in real time and act as a master kill switch.

Following the 1% risk rule at the portfolio level, not just per trade, is one of the simplest guardrails a trader can install. Top prop firm traders know this. It’s why the most successful automated accounts rarely blow up, even when individual strategies underperform.

Pro Tip: Adaptive EAs that can read volatility conditions and self-suspend during abnormal market behavior add a powerful layer of portfolio protection. Look for systems that include ATR-based filters or news avoidance logic baked into their code, not bolted on afterward.

The combination of automated risk management tips with genuine strategy diversification is where real account longevity comes from. Neither element alone is sufficient.

Why gold, Forex, and cross-asset portfolios behave differently

Real-world data makes the case for careful cross-asset portfolio construction better than any theoretical argument. When you look at historical stress periods, the performance difference between diversified and concentrated portfolios is striking.

Cross-asset portfolios with gold can outperform more concentrated portfolios, but the effectiveness of that protection varies with regimes and correlation shifts. During the 2008 financial crisis, gold held its value while equities crashed. During the March 2020 COVID selloff, gold initially dropped alongside everything else before recovering sharply.

Gold’s hedge effectiveness shows regime-dependent anti-persistence and shifting correlation during crisis events, which means its protective role is not constant. It strengthens or weakens depending on what’s driving the stress.

| Market environment | Gold behavior | Forex EA diversification impact |

|---|---|---|

| Equity bear market | Strong hedge | Medium benefit |

| Dollar weakness | Strong hedge | Moderate benefit |

| Liquidity crisis | Weak hedge | Low benefit |

| Low volatility range market | Neutral | High benefit from mean reversion |

| Trend-driven Forex market | Neutral | High benefit from trend systems |

Factors that shift gold’s hedge effectiveness across time include:

- Real interest rate levels: When real rates are negative, gold tends to perform strongly. When real rates rise sharply, gold weakens.

- Dollar strength cycles: Gold typically moves inversely to the dollar, but this relationship breaks down during broad risk-off events.

- Central bank buying and selling: Large-scale institutional flows can override typical correlation patterns for extended periods.

- Market liquidity conditions: In a genuine liquidity crunch, correlations across all assets converge toward 1.0 as everyone sells what they can.

Understanding these dynamics is essential for traders who want to use gold trading optimization tips effectively. Gold EAs that work beautifully in one macro regime can underperform significantly in another. A portfolio that includes examples of trading systems designed for different macro conditions will naturally fare better over full market cycles.

Practical frameworks: How to build robust, diversified trading portfolios

Now for the actionable part. Building a genuinely diversified automated portfolio requires structured thinking, not just trial and error.

Maximizing diversification is often superior to simply minimizing risk, especially when market conditions are changing and correlations are uncertain. The goal is to capture uncorrelated return streams while keeping individual position sizes small enough that no single failure is catastrophic.

Here are the core principles for a robust trading portfolio:

- Identify distinct edge types: Your portfolio should include at minimum a trend-following strategy, a mean-reversion strategy, and ideally a volatility-breakout strategy. These three edge types respond differently to market conditions.

- Separate across market sessions: Some EAs perform best during the London session, others during New York or Asian hours. Session-based diversification adds a time dimension to strategy separation.

- Mix timeframes deliberately: A scalping EA and a swing-trading EA behave very differently even on the same instrument. Combining them reduces the chance of simultaneous large losses.

- Track strategy correlations monthly: Once a month, compare the equity curves of your active EAs over the last 30 trading days. If two strategies start showing high correlation, investigate why before the next market shock reveals the problem.

- Use forward-testing, not just backtesting: Backtested correlation is historical. Live correlation can shift quickly. Always validate portfolio behavior on recent live or demo data before committing full capital.

- Limit total open lot exposure: Define a maximum combined lot size across the full portfolio relative to account equity. This prevents individual EAs from inadvertently building positions that overwhelm your buffer.

Staying current with automation trends for trading strategies matters here too. AI-driven EAs and adaptive systems are increasingly capable of detecting correlation shifts in real time and adjusting their behavior accordingly. That kind of built-in intelligence adds resilience that static systems can’t match.

Pro Tip: Review your portfolio’s correlation matrix every 30 days, not just when performance drops. Hidden overlaps often appear slowly, well before they cause visible damage to your account. Catching them early is far cheaper than discovering them during a drawdown.

The uncomfortable truth most traders miss: Even ‘diversified’ portfolios break if you overlook hidden risks

Here’s what experienced traders rarely say out loud: the moment you feel most confident in your portfolio structure is often when you’re most exposed. This is not pessimism. It’s a pattern that repeats across all automated trading environments.

Correlations and hedge effectiveness can rise sharply in stress regimes, meaning that a diversified set of strategies can still fail together if they share hidden common risk drivers. The trap is that those hidden drivers are invisible during normal markets.

What are these hidden common risk drivers? Things like: shared sensitivity to USD liquidity events, overlapping leverage exposure, common broker slippage during news, or simply the fact that every trend-following EA on every instrument will get stopped out when the dollar moves 2% in 30 minutes.

Surface-level diversification, the kind that looks great in a backtest or a spreadsheet, breaks down during once-in-a-decade events. The COVID crash of March 2020, the 2022 Ukraine invasion currency spikes, and the March 2023 banking crisis all created conditions where previously uncorrelated strategies suddenly moved together.

The practical response isn’t to avoid diversification. It’s to build portfolios that are stress-tested specifically against extreme scenarios. Run your portfolio through simulated 2008 conditions, 2020 conditions, and 2022 conditions. Check which EAs would have survived, which would have been flat, and which would have been catastrophic. Then size accordingly.

We believe that “set and forget” diversification is one of the most dangerous illusions in automated trading. The system advantages of automated portfolios are real, but they require ongoing oversight to stay effective. Markets evolve, correlations shift, and the edge that worked for 18 months may already be decaying. Treating portfolio diversification as a quarterly review task, not a one-time setup, is what separates durable accounts from ones that eventually blow up despite looking well-structured.

Take the next step: Build your diversified trading system

If you’ve made it this far, you now have a clearer picture of what genuine strategy diversification looks like and why surface-level approaches fall short. The next step is finding the right tools to put these principles into practice.

At FxShop24, we’ve built a library of trading software for Forex and Gold specifically designed for traders who want more than just a single-edge EA. Whether you’re building a multi-strategy portfolio from scratch or looking to add uncorrelated systems to what you already run, our catalog covers trend, mean-reversion, and volatility-based approaches tested on MT4 and MT5. Explore our automated futures trading systems guide for a deeper look at how automated portfolios are structured for long-term performance across asset classes. Every tool comes with lifetime updates and full installation support.

Frequently asked questions

What is the single biggest benefit of diversification in trading?

It reduces the risk of large drawdowns and smooths out returns by ensuring not all strategies lose at once. Combining approaches that respond to different market regimes and carry low correlation is what produces more consistent equity curves over time.

Can running multiple EAs on the same account backfire?

Yes, absolutely. If the EAs are correlated or lack portfolio-wide risk limits, losses across all systems can compound simultaneously, making the total drawdown far worse than any single EA would produce alone.

Does gold always act as a safe haven in trading portfolios?

No. Gold’s hedge role is regime-dependent and shifts during major crisis events, meaning it can sell off alongside equities during liquidity crunches before reasserting its safe-haven behavior.

What’s a common pitfall when diversifying trading strategies?

Believing that trading more symbols or running more EAs equals real diversification, when correlation may still be high. Diversifying across instruments only works when those instruments genuinely behave independently of each other.

How frequently should portfolio correlations be reviewed?

At minimum, monthly. Correlations can rise sharply during stress regimes, so what looked uncorrelated in calm markets may show dangerous overlap during the next major volatility event.