14

Jun

The Role of Backtesting in Strategies: 2026 Guide

TL;DR:

- Backtesting applies trading rules to historical data to assess strategy performance before risking real capital. It reveals if a strategy had a statistical edge in the past but cannot predict future success, emphasizing the importance of thorough validation. Proper backtesting requires sufficient trades, elimination of biases, and forward testing to build reliable, durable trading strategies.

Backtesting is defined as the process of applying a set of trading rules to historical market data to measure how a strategy would have performed before risking real capital. For forex and commodity traders, the role of backtesting in strategies is not optional. It is the minimum standard of due diligence separating disciplined traders from gamblers. Tools like the TradeZella backtesting engine, platforms like MetaTrader 4 and MetaTrader 5, and metrics like the Sharpe ratio all feed into a process that tells you one critical thing: whether your strategy ever had an edge at all.

What does backtesting reveal about strategy viability?

Backtesting shows whether a strategy had a statistical edge in the past. It does not predict future returns. That distinction matters more than most traders realize.

A failed backtest predicts poor results with near certainty. A positive backtest, however, is only a prerequisite for further testing. Think of it as a filter, not a forecast. If a strategy cannot survive historical data, it has no business touching live capital.

For a backtest to carry statistical weight, 200 trades minimum are required to establish credible evidence of a trading edge. Fewer trades produce results that are too easily explained by luck. A sample of 200+ trades across varied market conditions gives you something worth analyzing.

Here is what a well-run backtest can and cannot tell you:

- Can tell you: Whether entry and exit rules produced positive expectancy historically

- Can tell you: The maximum drawdown, win rate, and average risk-to-reward ratio

- Can tell you: How the strategy behaved across trending and ranging markets

- Cannot tell you: Whether those conditions will repeat in the future

- Cannot tell you: Whether the edge is real or a product of overfitting to past data

One metric that trips up traders consistently is the Sharpe ratio. A Sharpe ratio above 2 in liquid markets is a red flag, not a trophy. Results that clean almost always indicate the strategy was fitted to the data rather than derived from a genuine market inefficiency.

Pro Tip: Before you analyze any backtest output, ask yourself: “Did I define every rule before running this test?” If you adjusted parameters after seeing results, the data is contaminated and the output is meaningless.

How do out-of-sample and walk-forward testing improve reliability?

Out-of-sample testing and walk-forward validation are the two methods that separate serious strategy development from wishful thinking. Both address the same core problem: a strategy that fits historical data perfectly may have zero predictive value going forward.

Out-of-sample testing works by splitting your historical data into two segments. You develop and optimize the strategy on the first segment (in-sample data), then test it untouched on the second segment (out-of-sample data). The out-of-sample segment acts as a proxy for live trading conditions the strategy has never seen.

Walk-forward validation takes this further with a rolling process:

- Select a fixed historical window (for example, 12 months of data) and optimize the strategy on that window.

- Test the optimized rules on the next unseen period (for example, the following 3 months).

- Record the out-of-sample results without making any adjustments.

- Roll the window forward and repeat the process.

- Compile results across all iterations to assess overall robustness.

Repeating this process 5 to 10 times gives a far more reliable estimate of whether a strategy is genuinely robust or simply overfitted to a specific data window. Each iteration is an independent test. Consistent performance across all of them builds real confidence.

Experienced traders expect out-of-sample performance to be lower than in-sample performance. That degradation is normal. What matters is whether the strategy remains profitable and within acceptable drawdown limits across multiple windows. A strategy that collapses completely in out-of-sample testing is telling you something important: the rules were tuned to noise, not signal.

This validation pipeline is especially relevant for forex traders working across EUR/USD, GBP/JPY, or XAU/USD, where market regimes shift with central bank policy cycles and macroeconomic conditions. A strategy validated only on 2020 data may not survive 2024 volatility patterns.

What backtesting pitfalls destroy reliable results?

Backtesting results are systematically overstated. Survivorship, lookahead, and optimization biases all inflate the numbers you see on screen. Understanding each one is not academic. It is survival.

The three most damaging biases:

- Survivorship bias: Testing only on instruments or strategies that are still active today ignores the ones that failed. This skews results toward unrealistic profitability.

- Lookahead bias: Using data in the backtest that would not have been available at the time of the trade. A common example is using the closing price of a candle to trigger an entry that would have had to occur before that candle closed.

- Optimization bias (curve fitting): Tweaking parameters until the strategy looks perfect on historical data. The result is a strategy that describes the past with precision and predicts the future with none.

There is also what some analysts call “liar’s bias.” This is the cumulative effect of small, seemingly reasonable adjustments made during testing that collectively produce a strategy that never existed in real trading conditions.

Bias Type vs. Impact on Live Performance:

| Bias Type | Source | Typical Live Impact |

|---|---|---|

| Survivorship bias | Incomplete data sets | Overstated win rates |

| Lookahead bias | Incorrect data timing | Trades that cannot be replicated |

| Optimization bias | Excessive parameter tuning | Strategy collapses out-of-sample |

| Unmodeled costs | Missing slippage and spread | Returns lower than projected |

Unmodeled transaction costs are a silent killer. Slippage, spread widening during news events, and swap costs on overnight positions all eat into returns that look clean in a backtest. The practical fix is to discount backtest returns by 30–50% and inflate projected drawdowns by 1.5–2x before making any deployment decision. That adjustment alone prevents a large number of costly mistakes.

Keeping adjustable parameters below five is a reliable guardrail against curve fitting. Every additional parameter you add gives the strategy more ways to describe the past and fewer ways to predict the future.

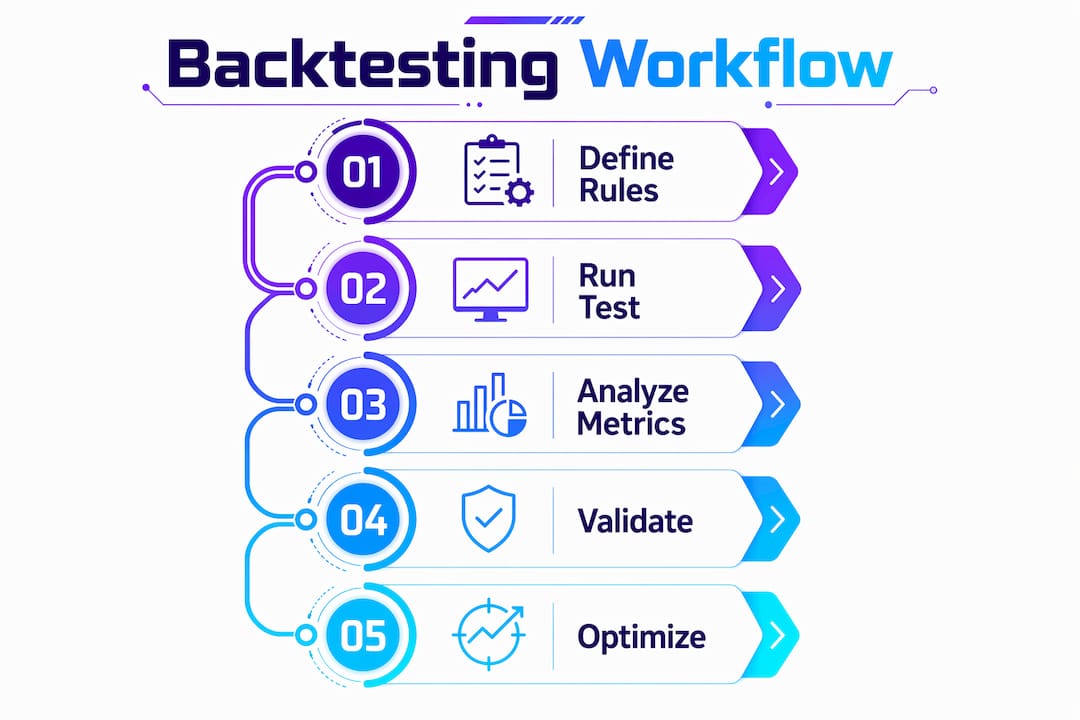

How should traders build backtesting into their workflow?

Backtesting works best when it is treated as hypothesis elimination, not performance prediction. The goal is to discard bad strategies quickly and cheaply before they cost you real money in live markets.

A disciplined workflow follows this sequence:

- Define every rule in writing before touching data. Entry conditions, exit conditions, position sizing, and stop placement must all be specified. Vague rules produce vague results.

- Gather sufficient data. Test across at least two distinct market regimes, such as a trending period and a ranging period. For forex pairs like EUR/USD, five or more years of tick data provides meaningful coverage.

- Run the initial backtest and record results without adjustments. Do not optimize at this stage. You are testing the hypothesis, not building the best-looking equity curve.

- Apply out-of-sample and walk-forward validation as described above before drawing any conclusions about viability.

- Complement backtesting with paper trading and live monitoring. A strategy that passes historical validation still needs to prove itself in real-time execution before scaling up capital.

Locking rules before validation and keeping parameters below five are the two most effective controls against data contamination. Both require discipline. The temptation to tweak after seeing results is the single most common reason traders end up with strategies that look great on paper and fail immediately in live conditions.

One framework worth adopting is the Asymmetric Scorecard approach, which tracks live execution quality alongside historical validation. This method monitors whether your live trades are actually executing according to the rules you backtested. It closes the gap between simulation and reality, which is where most strategies break down.

Pro Tip: Treat every backtest as a question, not an answer. The question is: “Does this strategy have enough evidence to justify further testing?” If yes, move to out-of-sample validation. If no, discard it and move on.

For traders using algorithmic trading basics to build automated systems, this workflow integrates directly into the expert advisor development cycle on MT4 and MT5. The same principles apply whether you are coding a scalper for gold or a trend-following system for crude oil futures.

The hard truth is that fewer than 3 out of 50 strategies make it from initial backtesting through live sessions to production deployment. That number should not discourage you. It should calibrate your expectations and remind you that the filtering process is working exactly as intended.

Key takeaways

Backtesting is a mandatory filter for eliminating losing strategies, not a tool for predicting profits, and its value depends entirely on disciplined rule-setting, sufficient data, and rigorous out-of-sample validation.

| Point | Details |

|---|---|

| Minimum trade sample | Test at least 200 trades to achieve statistically credible evidence of a trading edge. |

| Treat results as a filter | A positive backtest is a prerequisite for further testing, not a green light for live deployment. |

| Validate beyond in-sample | Use walk-forward testing across 5–10 windows to confirm robustness before going live. |

| Discount all projections | Cut projected returns by 30–50% and multiply drawdowns by 1.5–2x to account for real-world costs. |

| Lock rules before testing | Define every entry, exit, and sizing rule in writing before running any backtest to prevent data contamination. |

Backtesting is a sanity check, not a crystal ball

From where Fxshop24 sits, the biggest mistake traders make with backtesting is not running bad tests. It is trusting good-looking tests too much.

A beautiful equity curve is not evidence of a real edge. It is evidence that someone spent enough time optimizing parameters to make historical data tell the story they wanted to hear. The traders who survive long enough to build real track records are the ones who interrogate every metric, question every assumption, and treat a passing backtest as the beginning of the process, not the end.

The failed backtests are actually the valuable ones. Every strategy you eliminate in simulation is a strategy that cannot destroy your account in live trading. That is not failure. That is the system working.

What Fxshop24 has seen consistently is that traders who complement their backtesting with paper trading and live execution monitoring build far more durable strategies than those who go straight from simulation to live capital. The gap between how a strategy behaves in a backtest and how it behaves in real-time execution is always larger than expected. Slippage, emotional interference, and market microstructure all create friction that no backtest fully captures.

The right mindset is skepticism by default. If a backtest looks too good, it probably is. If the Sharpe ratio is above 2 in a liquid market, start looking for the bias before celebrating the result. The traders who approach backtesting this way are the ones who eventually find strategies worth trading.

— Fxshop24

Build on solid backtesting with proven automated systems

Every expert advisor and trading robot worth deploying starts with exactly the kind of rigorous backtesting process described in this article. The difference between an EA that holds up in live markets and one that collapses after two weeks is almost always the quality of its validation history.

Fxshop24 offers a full catalog of automated futures trading systems built and tested for MetaTrader 4 and MetaTrader 5, covering forex pairs and gold markets. Each system comes with documented performance data, prop firm compatibility, and lifetime updates. If you want to skip the trial-and-error phase and deploy systems that have already survived the validation gauntlet, explore the Fxshop24 marketplace. You can also review the full guide on backtesting trading robots to apply these principles directly to MT4 and MT5 automation.

FAQ

What is backtesting in trading?

Backtesting in trading is the process of applying a defined set of trading rules to historical market data to evaluate how the strategy would have performed. It provides statistical evidence of a potential edge before any real capital is risked.

Why is backtesting important for forex traders?

Backtesting filters out losing strategies before they cost real money. A strategy that cannot produce positive results on historical forex data has almost no chance of succeeding in live markets.

How many trades do you need for a valid backtest?

Industry standards require a minimum of 200 trades to achieve statistically significant backtesting results. Fewer trades produce outcomes too easily explained by random chance rather than genuine edge.

What is the biggest risk in backtesting strategies?

Overfitting, also called curve fitting, is the most damaging risk. It occurs when a strategy is tuned so precisely to historical data that it loses all predictive value in live conditions.

How does walk-forward testing differ from standard backtesting?

Standard backtesting applies rules to a single historical data set. Walk-forward testing repeats the optimization and validation process across multiple rolling windows, providing a more reliable measure of whether a strategy is genuinely robust or simply fitted to one specific period.