11

Jun

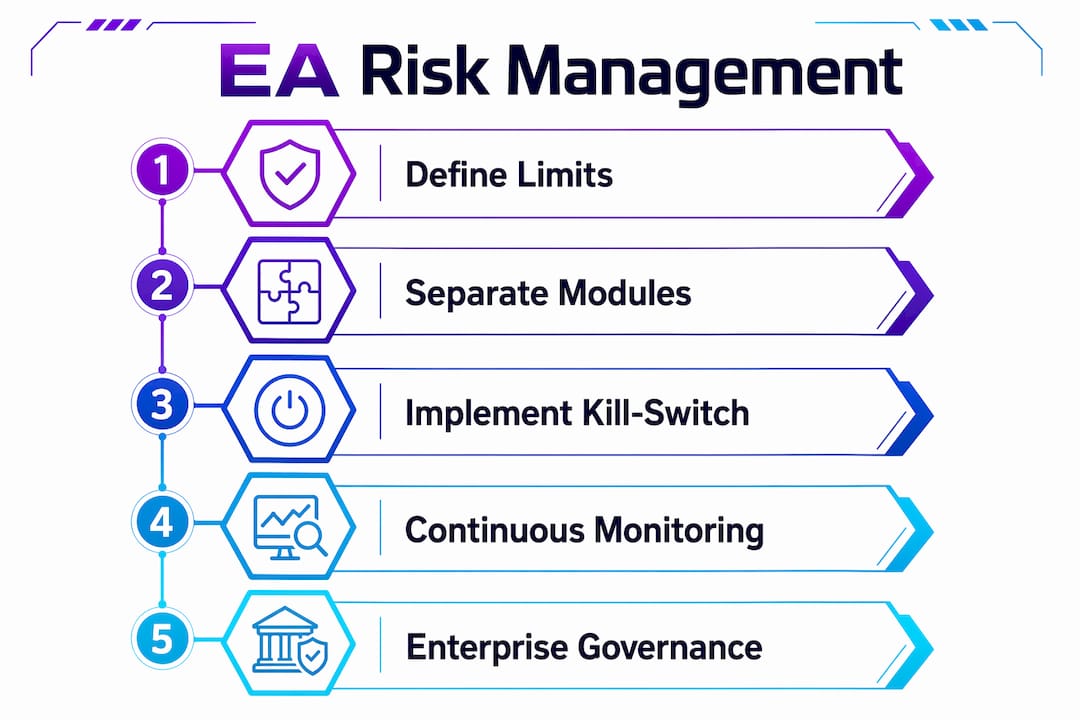

The Role of Risk Management in EA Trading Systems

TL;DR:

- Effective risk management in EAs involves separating loss control modules from signal logic to prevent unintentional disabling during live trading.

- Calibrating kill-switch thresholds tighter than historical worst draws and implementing manual resumption gates improve long-term survivability.

- Applying iterative frameworks like ISO 31000 ensures ongoing adaptation and continuous monitoring, critical for evolving market conditions.

Risk management in an Expert Advisor (EA) is the systematic process of limiting losses and controlling risk exposure through modular, enforceable rules embedded directly within automated trading systems. Most traders focus on signal quality, entry logic, and backtested returns. The traders who survive long enough to compound those returns are the ones who treat risk control as a separate, non-negotiable layer of their EA architecture. The role of risk management in EA design is not to generate profit. It is to prevent a single bad week from erasing months of gains. Tools like circuit breakers, drawdown limits, and modular kill switches are the mechanisms that make that protection real.

What is the role of risk management in an automated Expert Advisor?

Risk management in an EA operates as a dedicated module that is architecturally separate from the signal generation logic. In MQL5 EA design, risk management is separated as a module enforcing loss limits including daily loss, drawdown, and trade count thresholds. This separation matters because it means you can update, test, or disable risk rules without touching the underlying trade logic, and vice versa.

The risk control module does not decide when to buy or sell. It decides when to stop. When a predefined trigger fires, such as a daily loss threshold, a maximum drawdown level, or a streak of consecutive losing trades, the module pauses all trading activity until conditions are reviewed. This is the EA equivalent of a circuit breaker on a stock exchange. It prevents a bad signal from becoming a catastrophic loss.

Practical circuit-breaker conditions in a well-designed EA include:

- Daily loss limit: Trading halts when realized or floating losses exceed a fixed percentage of account balance within a calendar day.

- Maximum drawdown: All positions are closed and new entries are blocked once equity drawdown breaches a hard-coded threshold.

- Consecutive loss count: After a defined number of losing trades in sequence, the EA pauses to prevent revenge-trading behavior in automated form.

- Spread spike filter: The EA skips entries when broker spread exceeds a set multiple of the average, protecting against execution slippage during news events.

Separating risk control as a survival mechanism distinct from signal generation also simplifies testing and maintenance. You can stress-test your kill switch in isolation without running a full backtest of the entire strategy.

Pro Tip: Build your risk module as a standalone function or class in MQL5. Pass account equity and balance as inputs. This lets you unit-test the kill switch logic independently before attaching it to any live signal.

How do portfolio-level kill switches and drawdown limits improve EA risk control?

A single-trade stop loss protects one position. A portfolio-level kill switch protects your entire account. These are different problems requiring different solutions, and conflating them is one of the most common mistakes in automated trading system design.

Portfolio kill switches halt all trading when cumulative drawdown breaches calibrated daily or weekly thresholds. The daily counter resets each morning, while the weekly counter accumulates across all five trading sessions. When either threshold is breached, the EA stops opening new positions for the remainder of that period. This prevents a single bad day from compounding into a destroyed account.

Calibrating those thresholds correctly is where most traders underinvest their attention. The process should follow these steps:

- Run your full backtest and identify the single worst drawdown period in the historical data.

- Set your kill-switch threshold tighter than that worst-case figure. Backtest worst scenarios calibrate circuit breaker thresholds, ensuring live trading halts before the strategy exceeds its known statistical edge.

- Separate daily and weekly counters in your code. The daily counter resets at midnight server time. The weekly counter must not reset until the trading week closes on Friday.

- Require a manual resume after a weekly threshold breach. Automatic resets at the start of a new week invite the same losing behavior to repeat immediately.

The manual resume requirement is not a technical constraint. It is a discipline mechanism. When a human must actively decide to restart trading after a significant drawdown, it creates a natural review gate. That gate is where you ask whether the market regime has changed, whether the EA’s edge is still intact, and whether the position sizing remains appropriate.

Pro Tip: Log every kill-switch trigger with a timestamp, the triggering metric, and the account equity at the moment of halt. After three months, review those logs. Patterns in when and why your circuit breakers fire are more informative than any backtest report.

Why is continuous risk monitoring and the ISO 31000 framework important for EA risk management?

Risk management is not a configuration you set once at deployment. Markets change, volatility regimes shift, and the statistical edge your EA was built on can erode without warning. ISO 31000 defines an iterative risk management process with continuous monitoring and review, making risk management an ongoing practice rather than a one-time setup. The six-step process covers communication, scope setting, risk identification, analysis, evaluation, and treatment, all operating under a continuous monitoring layer.

For EA traders, applying ISO 31000 principles means treating your risk rules as living components of the system rather than static parameters. Specific practices include:

- Scheduled threshold reviews: Revisit kill-switch levels and position sizing rules at least monthly, or after any significant market regime shift such as a central bank policy change or a volatility spike in gold or forex pairs.

- Monitoring and review cadence: Track real-time metrics including equity curve slope, average trade duration, and win rate deviation from backtest expectations. A 15% drop in win rate is a signal to review, not ignore.

- Stakeholder communication: If you manage capital for others or trade through a prop firm, document your risk rules and share threshold changes with relevant parties. Undocumented changes create accountability gaps.

- Adaptive treatment: When a new risk is identified, such as a broker changing its swap policy or a new correlation appearing between two currency pairs your EA trades, update the risk treatment rules before the next live session.

ISO 31000’s iterative model encourages treating risk controls as living system components, which is essential for adapting to evolving market regimes. An EA that ran profitably through 2023 low-volatility conditions may need entirely different drawdown thresholds in a high-volatility 2026 environment. The framework gives you a structured reason to revisit those settings rather than assuming they remain valid indefinitely.

You can apply this same discipline to scaling automated trading across multiple instruments, where regime changes in one market can affect correlated positions across your entire portfolio.

How can enterprise-level risk registers and governance improve EA portfolio management?

Enterprise risk management (ERM) frameworks treat risk as a structured, documented, and escalatable concern rather than an informal judgment call. Applying that same rigor to an EA portfolio transforms risk management from a background process into a visible governance function.

NIST integrates cybersecurity risks into ERM via risk registers that roll up lower-level risks for enterprise-wide decisions. The same architecture applies to trading: individual EA-level metrics feed into a portfolio-level risk register that maps performance against investor risk appetite.

A practical EA risk register captures the following categories:

| Risk Event | EA-Level Metric | Portfolio Impact | Response |

|---|---|---|---|

| Daily loss breach | Account equity drop > 2% | Halt single EA | Manual review before resume |

| Spread spike | Spread > 3x average | Skip entry, log event | Review broker execution quality |

| Execution anomaly | Fill deviation > 5 pips | Flag for audit | Escalate to broker support |

| Drawdown trend | 3 consecutive losing days | Reduce position size | Reassess signal validity |

Mapping these events to investor risk appetite is what separates a professional EA operation from a hobbyist setup. When a prop firm sets a 5% maximum daily drawdown rule, your risk register should show exactly which EA-level triggers correspond to that limit and how they are enforced in real time.

Effective risk management requires operational cadence and accountability to avoid EA risk frameworks becoming sidelined concepts. Cadence means embedding risk review into your weekly workflow, not treating it as an emergency response. Accountability means assigning ownership of each risk metric to a specific person or process.

Pro Tip: Use a simple spreadsheet as your EA risk register if you are a solo trader. Log every kill-switch trigger, every threshold change, and every manual resume decision. After 90 days, you will have a documented risk history that no backtest report can replicate.

What practical challenges affect risk management implementation in automated trading?

Building a risk management framework on paper is straightforward. Keeping it intact under live market pressure is where most traders fail. Several specific technical and psychological challenges consistently undermine even well-designed risk controls.

Circuit breakers must be stateful and deterministic to avoid repeated misfires under rapid market conditions. Once triggered, a circuit breaker must halt trading and require a manual reset before resuming. A non-stateful implementation can re-evaluate the trigger condition on every tick, causing the EA to halt and resume repeatedly within seconds during volatile price action.

Misalignment between equity-based and balance-based drawdown triggers causes silent breaches and potential compliance issues for prop firm traders. A strategy can appear safe on realized balance while floating equity has already breached the prop firm’s limit. Always use equity-based triggers for prop firm compliance, not balance-based ones.

Additional challenges that demand attention include:

- Weekly counter mismanagement: Weekly drawdown counters must not reset daily. A bug that zeros the weekly counter at midnight allows the EA to breach its weekly limit in daily increments without ever triggering the intended halt.

- Portfolio correlation blindness: Portfolio-level sizing must account for correlations to prevent multiple low-risk trades combining into outsized portfolio drawdowns. Running three EAs on EURUSD, GBPUSD, and AUDUSD simultaneously is not three independent 1% risks. It is one correlated risk that can move against you in unison.

- Emotional override: Traders disabling circuit breakers during drawdowns due to emotional bias defeats the main protection risk controls provide. Adding social friction, such as requiring a second confirmation or logging the override reason, materially reduces the frequency of this behavior.

The importance of risk management in MT4 and MT5 environments extends to understanding exactly how your platform handles equity calculations during open positions, since the definition of equity varies between brokers and can affect when your triggers fire.

Key takeaways

Effective EA risk management separates loss-limiting logic from signal generation, uses stateful circuit breakers calibrated to historical drawdowns, and applies continuous monitoring under frameworks like ISO 31000 to keep risk controls relevant as market conditions change.

| Point | Details |

|---|---|

| Separate risk from signal logic | Build risk control as an independent module to simplify testing and prevent signal changes from disabling protections. |

| Calibrate thresholds to backtests | Set kill-switch levels tighter than your worst historical drawdown to protect capital from unknown regime shifts. |

| Use equity-based triggers | Always measure drawdown against floating equity, not realized balance, especially for prop firm compliance. |

| Apply ISO 31000 iteratively | Review and update risk thresholds monthly or after major market regime changes, not just at initial deployment. |

| Require manual resume gates | Force a human review after weekly threshold breaches to prevent automated systems from repeating losing behavior. |

Why risk management is the real edge in automated trading

After working with dozens of EA configurations across MT4 and MT5 environments, the pattern at Fxshop24 is unmistakable. The traders who blow accounts are rarely running bad signals. They are running good signals with no kill switch, or they disabled the kill switch during a drawdown because they were convinced the market was about to turn.

The uncomfortable truth is that most EA failures are not strategy failures. They are risk governance failures. The signal was fine. The position sizing was reasonable. But there was no hard-coded rule that said “stop here,” and so the losses compounded until the account was unrecoverable.

What actually works is treating the risk module as the most important part of the EA, not an afterthought. That means hard-coding thresholds that cannot be changed from the chart, requiring a deliberate manual action to resume after a significant halt, and reviewing those thresholds on a schedule rather than waiting for a crisis to prompt the review.

The traders who build this discipline into their systems early are the ones still trading two years later. The ones who skip it are the ones asking why their profitable backtest turned into a live account disaster. Risk management does not make your EA more profitable in a single week. It makes your EA survivable across hundreds of weeks, and survivability is what compounding requires.

— FxShop24

Explore professional EA systems with built-in risk controls

If you are ready to move from theory to implementation, Fxshop24 has the tools to get you there. The automated futures trading systems guide covers a curated selection of EAs built with modular risk controls, prop firm-compatible drawdown limits, and configurable kill-switch parameters for MT4 and MT5.

Every EA available through Fxshop24 is tested for real-world risk behavior, not just backtest performance. You can review forward test results, verify drawdown metrics, and confirm prop firm compatibility before purchase. For traders who want to understand the full software ecosystem before committing, the trading software overview breaks down every category of tool that supports risk management in automated trading environments. Demo testing is available on select products so you can validate kill-switch behavior in a live market environment before risking real capital.

FAQ

What does risk management do in an EA?

Risk management in an EA enforces loss limits by pausing or halting trading when predefined thresholds are breached, such as daily loss, maximum drawdown, or consecutive losing trades. It operates as a separate module from the signal logic, acting as a circuit breaker rather than a profit driver.

How should I calibrate my EA’s kill-switch thresholds?

Set your kill-switch thresholds tighter than the worst drawdown recorded in your backtest history. This protects capital from market regimes that fall outside the tested data range and prevents the EA from operating beyond its known statistical edge.

What is the difference between equity and balance drawdown triggers?

Equity drawdown measures floating losses including open positions, while balance drawdown only counts realized losses from closed trades. For prop firm compliance, equity-based triggers are required because a strategy can breach equity limits while balance remains technically intact.

Why does the weekly drawdown counter matter separately from the daily counter?

The daily counter resets each morning, but the weekly counter must accumulate losses across all five trading sessions without resetting. A coding error that zeros the weekly counter daily allows an EA to repeatedly breach its weekly limit in smaller daily increments without ever triggering the intended halt.

How does ISO 31000 apply to EA risk management?

ISO 31000 defines a six-step iterative risk process that includes continuous monitoring and review, making it directly applicable to EA systems where market conditions change over time. Applying its principles means treating kill-switch thresholds and sizing rules as living parameters that require scheduled review, not permanent settings.